Florida homeowners face water damage risks year-round, from hurricane season flooding to burst pipes during cold snaps. When disaster strikes, the first question most people ask is whether their homeowners insurance will cover the cost of water damage restoration. The short answer is: it depends on the source and cause of the damage.

Understanding what your policy covers before an emergency happens puts you in a much stronger position. This guide breaks down the types of water damage typically covered by homeowners insurance in Florida, what is usually excluded, and how to navigate the claims process so you can recover quickly and protect your property.

What Types of Water Damage Does Homeowners Insurance Cover?

Most standard homeowners insurance policies in Florida cover water damage that is sudden and accidental. This means the damage was unexpected and not caused by neglect or lack of maintenance.

Here are the most common covered scenarios:

- Burst or frozen pipes that suddenly crack and release water into your home

- Appliance malfunctions such as a water heater, washing machine, or dishwasher that fails unexpectedly

- Accidental overflow from a bathtub, sink, or toilet

- Storm damage where wind or hail damages your roof and allows rainwater inside

- Firefighting water damage caused by fire department efforts to extinguish a blaze

- Sudden plumbing failures like a supply line that breaks without warning

The key distinction is between sudden events and gradual problems. If a pipe bursts overnight and floods your kitchen, that is typically covered. If a slow leak under your sink has been dripping for months and finally causes visible damage, your insurer may deny the claim because the damage was preventable with routine maintenance.

What Water Damage Is Not Covered by Homeowners Insurance?

Knowing what your policy excludes is just as important as knowing what it covers. Most Florida homeowners policies do not cover:

Flood Damage

Standard homeowners insurance does not cover flooding from external sources like rising rivers, storm surge, or heavy rainfall that overwhelms drainage systems. Flood damage requires a separate flood insurance policy, typically through the National Flood Insurance Program (NFIP) or a private flood insurer. Given Florida’s hurricane exposure, flood insurance is essential for most homeowners in the Tampa Bay area.

Gradual or Maintenance-Related Damage

If water damage results from a slow leak, deteriorating plumbing, or a roof that has not been maintained, insurers often classify this as a maintenance issue rather than a covered peril. Regular inspections and prompt repairs help you avoid denied claims.

Sewer and Drain Backup

Water that backs up through sewers or drains is usually excluded from standard policies. However, many insurers offer sewer backup endorsements as an add-on to your existing policy. If your home has a basement or sits in a low-lying area, this endorsement is worth considering.

Mold Damage (in Some Cases)

Florida policies frequently limit or exclude mold coverage. Some policies cover mold if it results directly from a covered water event (like a burst pipe), but they may cap mold-related claims at a specific dollar amount. Acting quickly after water damage is the best way to prevent mold growth and avoid this coverage gap.

Ground Seepage

Water that seeps up through your foundation from underground sources is generally not covered by standard homeowners insurance.

Florida-Specific Insurance Considerations

Florida’s insurance landscape has unique challenges that every homeowner should understand:

Hurricane and Wind-Driven Rain

Wind damage from hurricanes is typically covered under your homeowners policy, including water damage caused by wind-driven rain entering through a damaged roof or broken windows. However, you may have a separate hurricane deductible that is higher than your standard deductible, often calculated as a percentage of your home’s insured value.

The Assignment of Benefits (AOB) Debate

Florida has seen significant changes around Assignment of Benefits agreements in the restoration industry. As a homeowner, you should understand your rights before signing any documents after a loss. Working with a reputable, IICRC-certified restoration company that practices direct insurance billing protects your interests while keeping you informed throughout the process.

Rising Premiums and Coverage Changes

Florida homeowners insurance premiums have increased significantly in recent years. Some insurers have reduced water damage coverage or added exclusions. Review your policy annually and discuss any changes with your insurance agent to avoid surprises when you need to file a claim.

How to File a Water Damage Insurance Claim in Florida

If you experience water damage, taking the right steps quickly can make a significant difference in the outcome of your claim:

1. Stop the Water Source

If possible, shut off the main water supply or the specific source of the leak. This prevents further damage and shows your insurer that you took reasonable steps to mitigate the loss.

2. Document Everything

Before moving anything or beginning cleanup, photograph and video all damaged areas. Capture wide shots of each affected room and close-ups of specific damage to walls, floors, ceilings, and personal belongings.

3. Contact Your Insurance Company

Report the damage to your insurer as soon as possible. Most Florida policies require prompt notification, and delays can complicate your claim. Keep a written record of every conversation, including dates, times, and the names of representatives you speak with.

4. Call a Professional Restoration Company

Contact an IICRC-certified water damage restoration company immediately. Professional restoration companies that offer direct insurance billing can begin mitigation right away while coordinating directly with your insurance adjuster. This reduces your out-of-pocket burden and ensures the work meets industry standards that your insurer expects.

5. Keep Records of All Expenses

Save receipts for temporary housing, meals, and any emergency repairs. These may be reimbursable under your policy’s additional living expenses (ALE) coverage if you are displaced from your home.

6. Get a Professional Damage Assessment

A certified restoration specialist can provide a detailed scope of work and moisture mapping documentation that supports your insurance claim. This professional assessment often helps ensure you receive fair compensation for the full extent of the damage.

Tips to Maximize Your Water Damage Insurance Claim

Filing a successful insurance claim requires preparation and attention to detail:

- Review your policy before disaster strikes so you understand your coverage limits, deductibles, and exclusions

- Maintain your home regularly and keep records of plumbing inspections, roof maintenance, and appliance servicing

- Act fast after damage occurs because insurers expect you to mitigate further loss

- Do not throw away damaged items until your adjuster has inspected them

- Get multiple repair estimates if your insurer’s initial offer seems low

- Consider hiring a public adjuster for large or disputed claims, as they can advocate on your behalf

When to Call a Water Damage Restoration Professional

Not all water damage is visible, and delaying professional help can turn a manageable situation into a major problem. Call a restoration professional if you notice:

- Standing water or saturated carpets and flooring

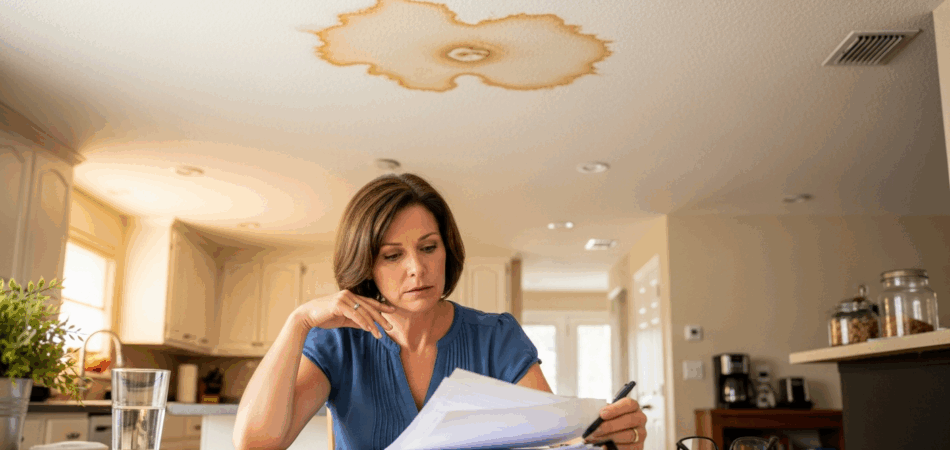

- Water stains on ceilings or walls

- A musty or damp smell that will not go away

- Visible mold growth on any surface

- Warped or buckling floors

- Peeling paint or bubbling wallpaper

Professional restoration companies use specialized equipment like industrial dehumidifiers, air movers, and moisture meters to detect hidden damage and ensure your home is thoroughly dried. This prevents secondary damage like mold growth, which can begin within 24 to 48 hours of water exposure.

Frequently Asked Questions

Does homeowners insurance cover water damage from a leaking roof in Florida?

It depends on the cause. If your roof was damaged by a covered peril like a hurricane or fallen tree, the resulting water damage is typically covered. If the roof leaked due to age or lack of maintenance, the claim will likely be denied. Regular roof inspections help prevent this issue.

Is mold from water damage covered by homeowners insurance in Florida?

Coverage varies by policy. Some Florida homeowners policies cover mold remediation if it results directly from a covered water damage event, but many cap mold coverage at $10,000 or less. The fastest way to avoid mold issues is to begin water damage restoration within 24 hours of the event.

Do I need flood insurance if I have homeowners insurance in Florida?

Yes. Standard homeowners insurance does not cover flood damage. Given Florida’s vulnerability to hurricanes, tropical storms, and heavy rainfall, flood insurance is strongly recommended for all homeowners in the Tampa Bay area, even if you are not in a designated flood zone.

How long do I have to file a water damage insurance claim in Florida?

Most Florida policies require you to report damage promptly, typically within a reasonable timeframe after discovery. While specific deadlines vary by insurer, it is best to contact your insurance company within 24 to 48 hours of discovering the damage. Delays can result in reduced payouts or denied claims.

Does homeowners insurance cover water damage from a burst pipe?

Yes, in most cases. A burst pipe is considered sudden and accidental damage, which is a covered peril under most standard homeowners policies. However, if the burst was caused by a known maintenance issue that you failed to address, coverage may be limited.

Protect Your Home and Your Investment

Water damage can happen to any Florida homeowner, whether from a sudden pipe burst, a storm, or an appliance failure. Understanding your insurance coverage before an emergency occurs gives you the knowledge to act quickly and protect your property.

If you are dealing with water damage right now, the most important step is to act fast. Contact a certified restoration company that can begin mitigation immediately, coordinate with your insurance provider, and guide you through the claims process from start to finish.

Drywizard Restoration and Drywall Inc. provides 24/7 emergency water damage restoration across the Tampa Bay area, with crews on-site in 45 minutes or less. As an IICRC-certified company, we work directly with your insurance company through direct billing so you can focus on your family while we handle the restoration and the paperwork. Call (813) 684-4800 for immediate help or contact us online for a free estimate.

Water Damage Restoration Across Tampa Bay

Drywizard Restoration & Drywall Inc. proudly serves homeowners and businesses throughout the Tampa Bay metro area. No matter where you are in the region, our IICRC-certified team can be on-site in 45 minutes or less. We provide 24/7 emergency water damage restoration in these communities:

- Water Damage Restoration in Valrico, FL

- Water Damage Restoration in Brandon, FL

- Water Damage Restoration in Riverview, FL

- Water Damage Restoration in Sun City Center, FL

- Water Damage Restoration in Citrus Park, FL

- Water Damage Restoration in Temple Terrace, FL

- Water Damage Restoration in Apollo Beach, FL

- Water Damage Restoration in Plant City, FL

- Water Damage Restoration in Lutz, FL

- Water Damage Restoration in Seffner, FL

Need immediate help? Call (813) 684-4800 for 24/7 emergency service anywhere in the Tampa Bay area.